By Evgenia, Henry, Nils and Owen

Many hard miles lie between technology breakthroughs and adoption. You’d be forgiven for thinking that cloud is “implemented” now that the hot topic baton has been passed to AI. In reality, only 30 percent of European businesses have migrated half of their workloads to the cloud (McKinsey). Obviously, transformations take a (very!) long time – until long after the novelty wears off. They require patient hand-holding through messy legacy stacks, processes, and cultures of real-world businesses.

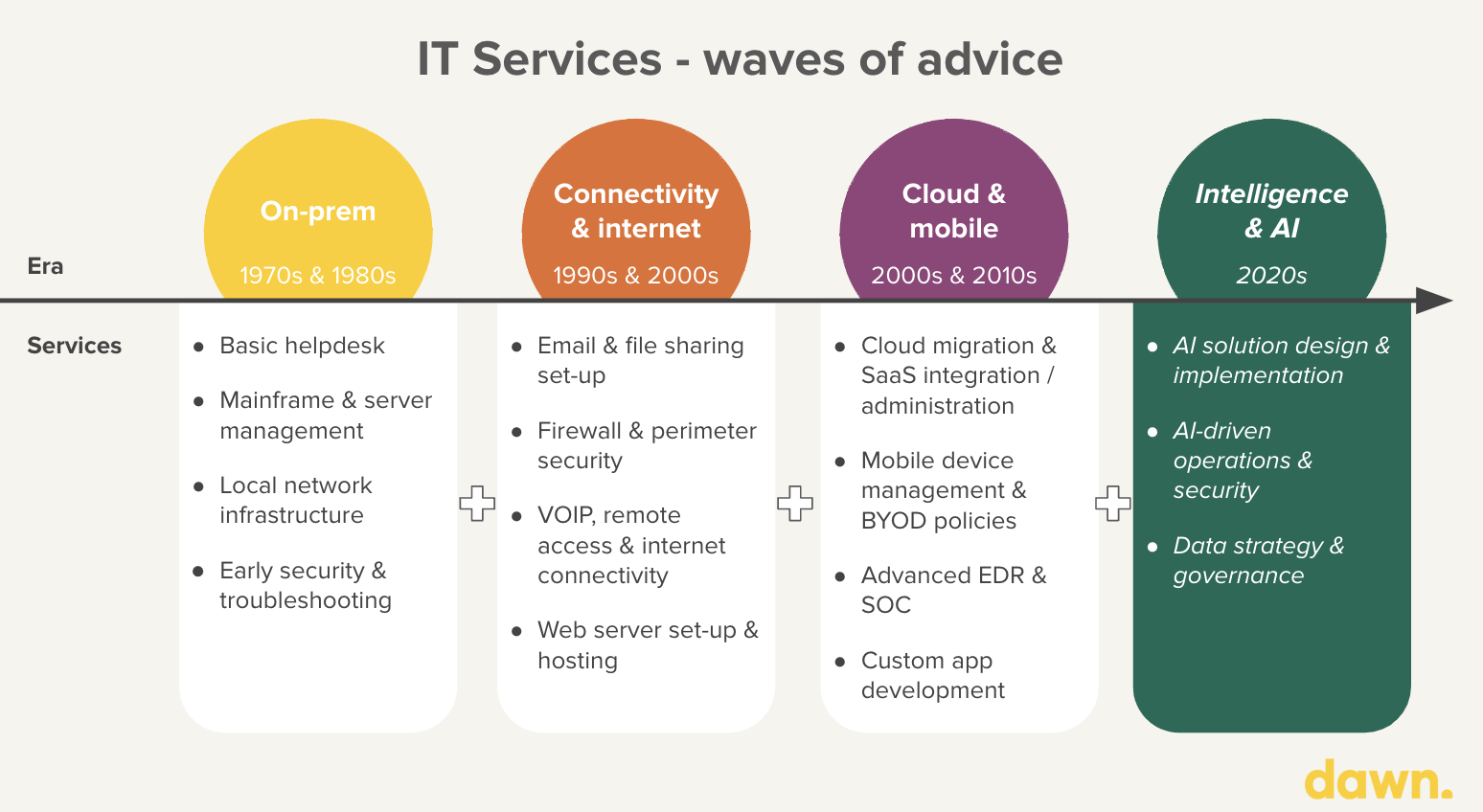

So often, this is done by an unsung hero: IT Services providers. Nearly invisible at times, they manage critical tech operations and act as both a thought and implementation partner for companies large and small navigating change in the technology landscape. They have existed as long as offices have had IT: from on-prem deployments and the original PCs, through the internet, cloud, and mobile revolutions. AI, too, will need this trusted advisor to implement change.

AI will of course, also disrupt IT Services in itself. It is natural territory for “service-as-a-software”. AI agents will automate full workstreams beyond just enabling them. We covered this approach in depth in our previous AI Agents article. Providers will harness them to deliver new and/or better services, at a cheaper price, near-instantly around the clock. They will package and deliver them for their clients – Nvidia CEO Jensen Huang recently talked about IT becoming the “HR for AI agents”. We agree: as a role for both in-house IT and managed services alike. Providers who don’t have AI and AI-enabled offerings risk being overtaken by those who do.

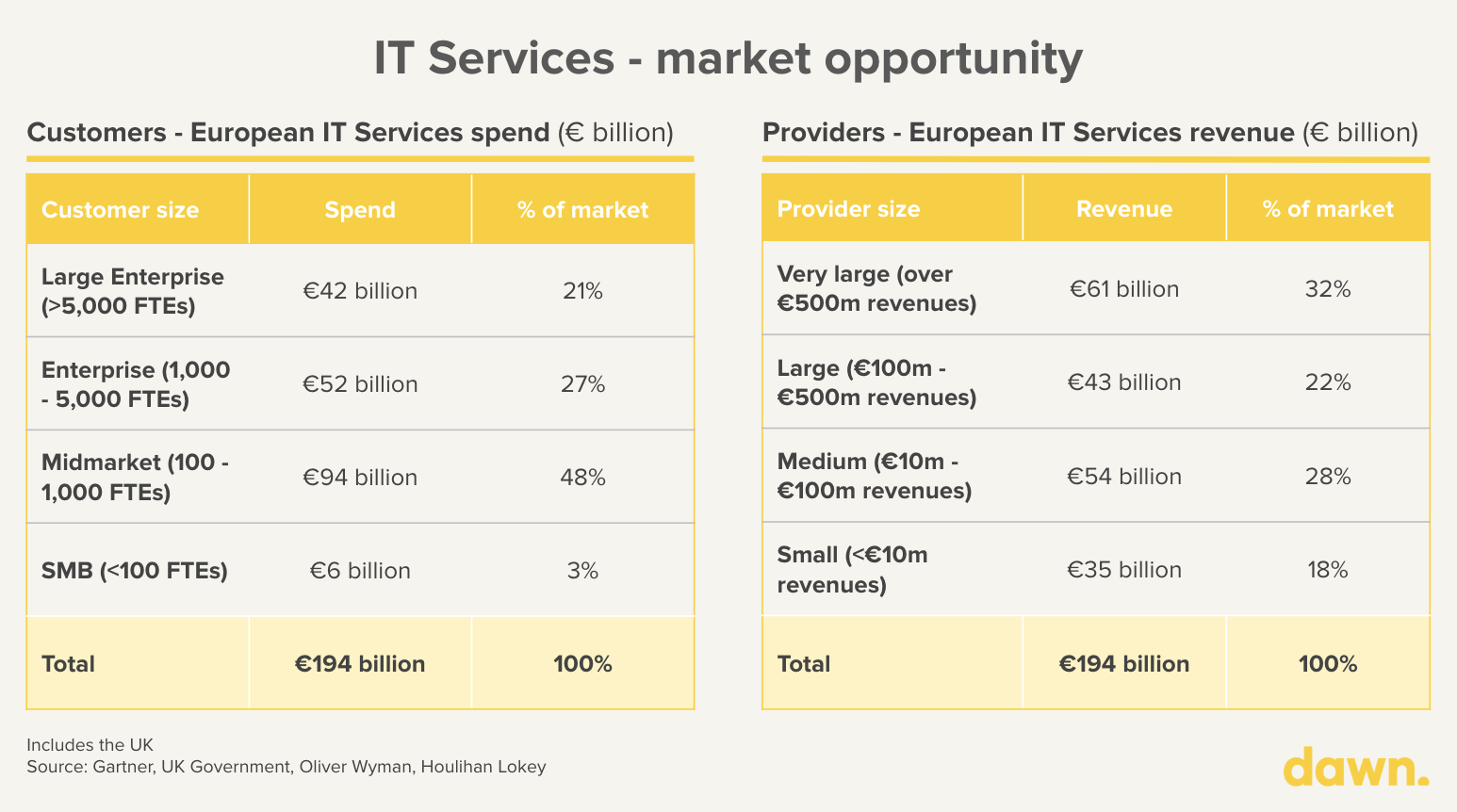

The prize is massive: we estimate that Europe alone spends €200 billion directly on these services. And providers influence even more spend indirectly by distributing and implementing software. We are excited by start-ups building their next-generation stack. We also highly recommend them as a channel for start-ups looking to distribute at scale, especially for the harder-to-reach midmarket and SMBs that lie outside of the world of technology start-ups.

We spoke to IT Services providers, end-customers, and their current software and reseller ecosystem to find out what the innovators and buyers on the ground expect to see happen as AI advances – and the emerging map of European software that will enable this opportunity too.

1. Europe’s €200 billion IT Services prize

Investors so often focus on software spend that we miss a simple fact: surrounding services can be an order of magnitude greater. Take ServiceNow: for every $1 spend on licences, they require $3 spend of services.

We estimate that Europe and the UK spend close to €200 billion (!) on IT Services. Each national market alone is huge. The UK represents over €50 billion spend, with more than 11,500 managed service providers (MSPs).

Customers – Customers of all sizes buy IT Services, and choose varying sophistication depending on their size and industry. Analogous to selecting software vendors – SMBs mostly look for a bundled platform, whilst Enterprises expect more sophisticated, best-of-breed offers. The level of industry regulation is also a good indicator of the complexity needed. Financial services and law firms, for example, often choose specialist offerings and spend up to three times more per head.

Midmarket spend is nearly half of the total, a large prize. At this scale (>100 employees), some will have built a small IT team, and will start to triage their operations between in-house and managed services. Traditionally, this has been a harder segment to crack for many MSPs – with requirements somewhere between the bundled platform and best-of-breed, depending on the exact size and industry. But success in this segment is also highly rewarded, with loyal and sticky customers.

In fact, churn is low regardless of size with contract lengths that regularly extend beyond five years in established relationships. As we implied earlier, start-ups partnering with IT services can unlock an avenue to sell into harder-to-reach and more traditional businesses. So often, this is where direct sales motions come unstuck.

Providers – The landscape of the providers closely resembles that of the market they serve. Around a third of the market’s revenues is dominated by a handful of global IT consultancies like Tata, IBM, Capgemini, and Accenture. Their economies of scale make them a universe unto themselves, often serving large enterprise customers with distinctly more in-house builds and a much higher proportion of consulting revenues.

However, we are also excited by the deep market beyond the giants too. Under half the market is serviced by providers with less than €100 million in revenues – often with both a geographical and industry GTM focus. They influence a huge amount of software spend directly (as buyers) and indirectly (as partners) in the midmarket and SMBs, including in traditional industries.

An enduring & growing proposition

The UK government expects a 12% growth rate for the MSP market over the next few years. The proposition is evergreen: customers want an expert to navigate the dizzying pace of change in technology, its risks, and regulations. This means:

- Focussing on your core business – e.g. “what makes your beer taste better” – customers see IT services as an enabling function, rather than part of their core offering.

- Buying expertise – customers find great IT skillsets hard to hire for and retain, especially around security.

- Insuring against disaster – customers want to rely upon this expertise to get the setup right and to monitor 24/7. This also means someone to call in the middle of the night and, in the worst case, to blame when major issues arise.

- Reducing the cost of IT & software spend – customers can leverage existing scaled partnerships with better pricing.

There are many different flavours of IT Services that address these needs. For simplicity, we cut offerings into four broad pillars:

- i) IT Infrastructure & Operations – managing end-user devices, networks, and helpdesks

- ii) Cloud & Application Services – building, migrating, modernising, and maintaining cloud-based solutions

- iii) Managed Security Services – providing continuous threat monitoring, vulnerability management, and incident response

- iv) Transformation & Compliance Services – offering strategic advice, training, and compliance & risk management

Behind each category is access to billions of dollars of spend and an opportunity for start-ups to drive innovation.

2. AI for IT Services & the Accenture case study

AI will bring new revenue streams and radically more profitable operating models.

To understand both, it’s first worth outlining the structural challenges that providers face:

- Pricing & margin pressures – offerings are well-defined and can be commoditised. Intense competition drives down pricing and margins – delivering the same SLA with fewer billable hours. Providers constantly look for ways to make their proposals to new and existing customers stand out (if possible, at a better price too).

- Talent scarcity – engineers, data experts, and cloud architects are gold-dust that are hard to find and retain. Security offerings (if present) might have to be sub-contracted to specialist MSSPs.

- Complex scaling – smaller providers struggle to scale FTEs and add management layers without creating diseconomies of scale – for example, inefficient hand-offs on tickets between teams.

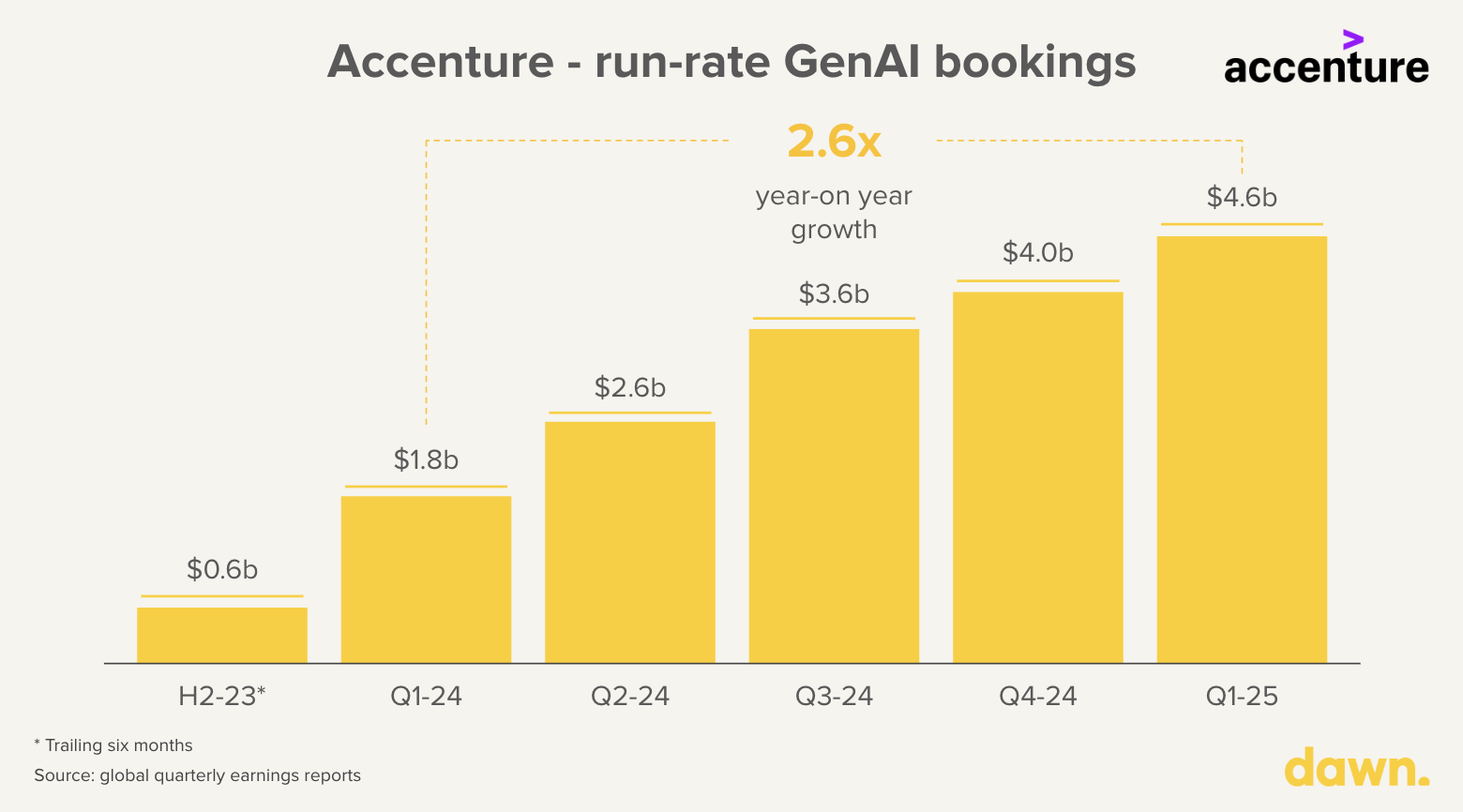

New revenue opportunities & Accenture’s $5 billion GenAI bookings

AI will play a large role in generating a huge swathe of lucrative, incremental projects. Accenture is an incredible early example of riding this wave, propelled by enterprise customers further along the maturity curve. They hit a run-rate of almost $5 billion (!) in global Generative AI bookings in Q1 2025 – now more than 5 percent of their total and almost tripling year-on-year. Some of this probably would have happened anyway, but likely much is newly urgent or possible. The majority of spend is on very practical applications: private GPTs / chatbots, helpdesks, internal knowledge search, and more (marketing automation, supplier evaluations). Only a minority are enabling custom models and in-house compute infrastructure. Getting the data governance right is a huge part of both, for example, only HR should be able to search for salary data. The cost of doing nothing drives urgency: employees might otherwise prompt public tools with highly sensitive data.

Accenture is just a single consultancy serving the enterprise tip of the market. Soon, the midmarket will join the AI gold rush and they’ll need IT Services to deliver on their ambitions. It will start simple: many customers first want help to get the most out of Microsoft Co-Pilot. And IT Services providers mostly want to service these use cases with off-the-shelf software – for AI start-ups, this means a huge swathe of dual GTM-and-implementation partners.

They might not even “sell the AI” to customers, but rather an outcome that implies a host of high-touch services: a new, better, and/or cheaper service.

A slight caveat to our optimism: we are in the very early days of defining the best use cases here. The Rand Corp still puts the failure rate of AI projects at over 80 percent. IT Services providers will be at the vanguard of testing and learning what works (and what doesn’t!).

AI-enabled operating models & the new landscape of IT tooling

Currently, the basic IT services stack is geared to reduce some of the administrative overhead:

- Professional Service Automation (PSA) system – for ticketing, project management, billing, and time tracking

- Remote Monitoring and Management (RMM) system – for device updates, patches, and proactive monitoring

- Back-ups – for disaster recovery of internal and client data

- Policy management – for documenting processes, incident response procedures, and data-handling policies

- Core security functionality – for endpoint security with MFA, antivirus, and firewalls

However, more sophisticated tooling and AI can dramatically increase the scope of automation and possible services – either directly (providers as customers) or indirectly (providers as implementers). Regardless, we expect a meaningful uplift to the bottom line.

Some painful processes ripe for improvement include:

Structuring, addressing and preventing support tickets – services mean bespoke approaches and set-ups. Context including documentation is often scattered, patchy and out-of-date. Worse, it might be non-existent or rather it exists in each employee’s head. Simple troubleshooting might then involve pulling in many other teammates and keeping 4-5 windows open (their Teams, MDM, IAM, HRIS etc.). AI agents will struggle without the proper context and will not meet the margin of error required for “prime time”.

In turn, basic level 1 tickets can represent more than 20 percent of total costs for an average MSP. Think, as basic as resetting your password. Time spent is not just resolution but also context gathering and switching. The average employee might resolve two hundred tickets a month, but better tooling (including context!) and AI agents could improve this into the thousands. Or, even better, they could improve the underlying tech and “prevent” more tickets. This needs a new system of record and knowledge gathering to be rolled out.

Example: Primo and Deeploi are rebuilding the full employee IT journey, from initial provisioning to offboarding. This easily represents 50 percent of the workload for SMB customers. Their all-in-one ecosystem of tooling sweeps away the web of RPA stitched-together systems, and avoids many of the usual manual interventions reconciling them. They are building a core “IT system of record”, like Rippling has done so successfully in HRIS.

Example: Way are clarifying, triaging, and autonomously resolving IT issues – all while maintaining security and compliance. In doing so, they are building a predictive analytics engine on what to change to reduce future tickets.

Running more sophisticated security operations – MSPs increasingly want to become credible MSSPs (often to unlock more midmarket customers) and, in turn, MSSPs want to focus on more value-add tasks. They want a toolkit for better threat detection, incident response, and vulnerability scanning. In future, this will even include authentication for non-human agents. Companies want to move from a reactive to a proactive security posture, that warns you in advance about the weakest links in your IT estate.

Example: Qevlar’s AI SOC analyst reduces the time to remediate alerts dramatically. MSSPs can sell this as a superior SLA, and MSPs have a lower upfront cost to adding incremental security capabilities – for example, managing email security is low-hanging fruit.

Managing applications and policies scalably across multiple tenants – IT Services providers can struggle with inconsistent standards and often have to manually push near-identical changes separately for each tenant – costing time and risking human error. Cross-tenant administration dramatically reduces time to deploy, gives real-time visibility, and upsell opportunities.

Example: Inforcer helps MSPs standardise policies and security baselines in the M365 ecosystem, scalably across all tenants. In the trend of MSPs becoming MSSPs, they can upsell features like Microsoft Secure Score as “new” functionality (despite being included in their client’s existing licence!). The Microsoft 365 ecosystem alone is huge: with around 350m users and 50 percent market share.

Becoming (and staying) compliant – SOC 2 and ISO 27001 requirements (amongst others) are growing in RFPs. They can make or break deals not just for Enterprises, but also for midmarket and SMB counterparties. Companies therefore see compliance as a strategic and revenue driver, not just a cost. MSPs and MSSPs leverage checklists from the likes of Drata and Vanta, but then have their own security tooling and manual services – for example, for pen testing. The next generation of tooling will combine compliance and cybersecurity into a single tool.

Example: Oneleet sells SOC-in-a-box. Their security-first package combines not just the checklists, but also the actual tests and third-party auditing services together into an easy-to-use platform – to dramatically reduce the time to certification.

Building or updating custom applications, integrations and workflows – custom software is a massive standalone market, for example, managing bespoke CRMs or ERPs. Today, around 20 percent of the time is spent on building software whilst the rest focuses on requirements engineering and maintenance. AI code generation will eventually condense this time drastically, and with higher maintainability will eventually have marginal cost trending closer to zero. This will unlock an endless long tail of automation use cases akin to a “supercharged RPA”.

Example: Cogna helps users discover and define opportunities for software, then deliver them. These are in production, not just prototypes – with dramatically lower development and maintenance costs.

Beyond this, we see huge potential to reinvent the back-office stack – with a direct effect on operating margins. We’ve already covered the huge potential for automation in sales & marketing, finance and HR, and developer productivity. An example for IT Services providers is better cross-tenant time tracking and billing infrastructure.

One large MSP expected generative AI to enable every part of their offerings and practices by the end of the decade. This is not entirely a free lunch. Customers are aware of productivity improvements that come with AI and Copilots and are already adjusting their pricing expectations – hence, we expect a shift away from billable hours to selling output.

With all this talk of automation, it’s worth restating where we started: the biggest value driver will be supercharging staff productivity – not replacing them entirely. They’ll be freed up from repetitive drudgery towards difficult edge-cases (as the HR of AI agents!) and, especially, the creative and interpersonal work involved in helping customers embrace change.

—

IT Services is just a single example of how AI will enable and disrupt every services industry. In many ways, these providers are the force multiplier: the thread that will weave it into the fabric of day-to-day operations.

We are very excited to hear from founders who are building around this space. If that’s you, please get in touch at: nils@dawncapital.com, owen@dawncapital.com, or evgenia@dawncapital.com, or henry@dawncapital.com.

P.S., we talked about IT Services being an incredible channel to distribute through providers to end-customers. If you are a founder thinking about this, we have a bunch of great learnings from our portfolio companies. Please do reach out, and we’ll be happy to share more.

Thank you to all those who contributed to this article. With special thanks to Mike Douglass and Jaime Higuera Mata for feedback on early versions of this article.