By Owen Brooks, Dan Chaplin and Nils Howland

Know Your Customer (KYC) software has become a cornerstone of modern compliance operations, leveraging biometrics and database checks. Know Your Business (KYB) on the other hand still remains relatively unsolved by software. Most KYC players have settled for outsourcing responsibility to third-party managed services, showing some reluctance to venture into this offering. It reflects key differences between KYC and KYB: more chaotic and varied datasets, the lack of “finality” in the evidence, and the amount at stake if elements are left ambiguous.

Engaging with business entities presents unique fraud considerations: who is in control, where they operate, their credit history, and how they are structured. KYB processes have to both deliver reliably during onboarding and on an ongoing basis as they consistently change and evolve. Failing to get this upfront onboarding and monitoring right is a major financial, regulatory, and reputational risk. Increasingly sophisticated fraud — for example, synthetic identities — and a more turbulent global geopolitical environment has only made such firms’ KYB processes more urgent and complex.

A lack of proven KYB software has resulted in companies taking a variety of directions to try and get to a solution from outsourcing the workload to third-party services, enduring cumbersome processes filled with back-and-forth communication and database checks, or building internal solutions as they scale up and internationally. If done manually, these are all vulnerable to significant human errors as well as an inherent lack of scalability.

We believe unlocking this KYB opportunity will be massive: the annual impact of global fraud now exceeds $1 trillion, according to LexisNexis. $46 billion is already spent on financial crime compliance in the US alone. And it is only getting worse — 91 percent of financial institutions have reported increased fraud rates according to Alloy’s Benchmark Report. Firms have been fined upwards of $100 million for inadequate oversight of compliance risks and record-keeping errors in recent years. And managing it successfully is a significant operational challenge — we’ve seen just recently here in Europe, Wise pausing new business onboarding as it struggled to cope with a significant backlog.

It’s not just a problem for financial services firms. KYB compliance extends to many other business propositions, marketplaces being just one example. Here, checks often need to be made on SMBs — 99 percent of all firms and 50 percent of GDP in high-income countries. According to Alloy, 29 percent of these don’t even have a website making this a significant headache.

Today, there is a clear opportunity for a next-generation solution to emerge.

The next generation of KYB

We’ve seen an array of emerging companies looking to rise to this challenge. These providers are differentiating across several dimensions: the quality and flexibility of their workflows, the depth of their analytics and risk capabilities, as well as access and standardisation of underlying business datasets.

As we see it, the strength of these platforms will be in both their usability for compliance analysts, and configurability to map to company’s individual processes, risk frameworks and customer sets — all of which are crucial given that reaching high levels of straight-through processing is just not possible for KYB as it is in KYC. Compliance decisions around businesses are hardly ever, if ever, clear cut. A first assessment will mostly deliver a set of “orange flags” that need to be reviewed.

Advanced risk detection and scoring engines are certainly one important step to improving efficiency (reducing false positives) and lowering perpetual risk exposure. Risk engines need to incorporate company and industry specific data and importantly contextualise it to enable faster decision-making for analysts. We have already seen companies emerging that solve this analytics challenge of managing myriad sources of risk data, like Quantexa — a Dawn portfolio company with a decision intelligence platform used for anti-fraud and analytics.

As important will be improvements in workflows for compliance analysts as KYB decisions will almost certainly remain human-in-the-loop. Business customers should not only have higher expectations of consumer-grade UI/UX, but also the ability to be agile in the configuration and orchestration of their KYB solution to their specific organisational risk frameworks and processes. Delivering fast, lower-touch and seamless user experience to maximise customer conversions while not trading off risk taken on (or regulatory requirements) is not easy. But it is crucial and extremely valuable — this due diligence takes up more than 40 percent of onboarding time for banks according to McKinsey. In turn, this may lead to different solutions tailoring to different KYB contexts such as marketplaces, e-commerce, supply chain management and beyond.

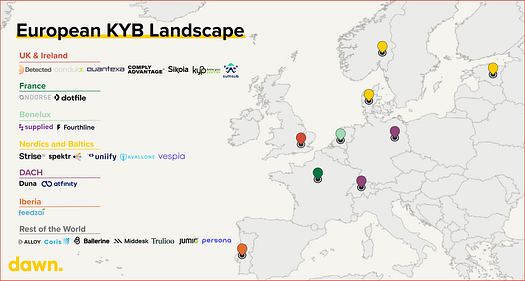

The European landscape

Europe is at the forefront of start-ups building in the KYB space, and we look forward to watching the sector develop. Some of the exciting new solutions on our radar include:

- UK and Ireland: Sikoia, Condukt, Detected, and KYP

- Benelux: Supplied and Fourthline

- France: Dotfile and Ondorse

- Nordics and Baltics: Spektr, Uniify, Strise, Avallone, and Vespia

- DACH: Duna and Atfinity

- Iberia: Feedzai

While KYB represents a complex and multifaceted challenge, the right solutions will transform the compliance landscape and seize a multi-billion dollar opportunity.

We’re keen to meet the companies taking on this challenge, and to hear more about your plans.

Please do get in touch with: nils@dawncapital.com and owen@dawncapital.com and dan@dawncapital.com.