The app development market is being turned upside down by AI. With the release of Claude Opus 4.6, coding agents are a practical reality. As such, we have moved away from a world where software is constrained by engineering bandwidth to one where software is constrained by clarity of intent, access to systems, and the ability to operationalise change.

The headline shift is simple: building software is getting cheaper and faster, but making it work inside an enterprise remains hard. In this piece, we highlight what enterprises need to get right to build successful applications, and what opportunities founders can capitalise on to support enterprises along this journey.

Why now for enterprise AI-native app development?

Enterprises are not trying to build one new app – they are trying to build dozens.

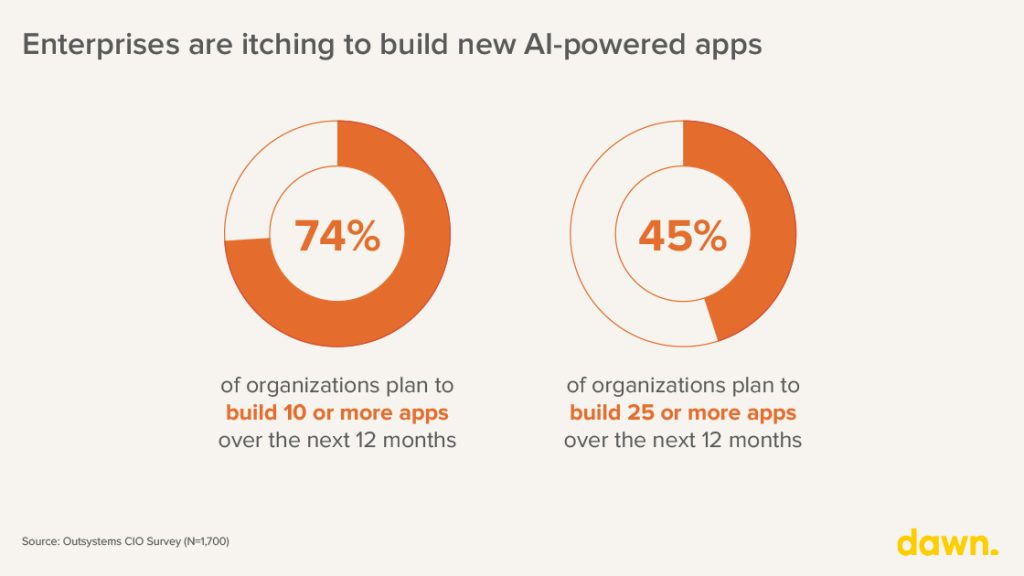

In an Outsystems survey of 1,700 CIOs, 74% of organisations planned to build 10 or more apps in the next 12 months, and 45% planned to build 25 or more. That demand is not driven by vanity projects. It’s driven by workflow fragmentation, regulatory pressure and customer experience expectations – and the realisation that AI is only truly valuable when it is embedded into day-to-day operations.

At the same time, leaders are getting more ambitious about what software should do. “Vibe-coding” has made prototyping feel instant, and it’s changing expectations inside businesses. Leaders now want to move from prototype tools to production-grade systems that scale reliably, and from low-context tools that work out-of-the-box to high-context builders that understand a company’s unique processes.

The result is a new category forming: AI-powered software that generates tailored working products inside complex organisations.

What is at stake?

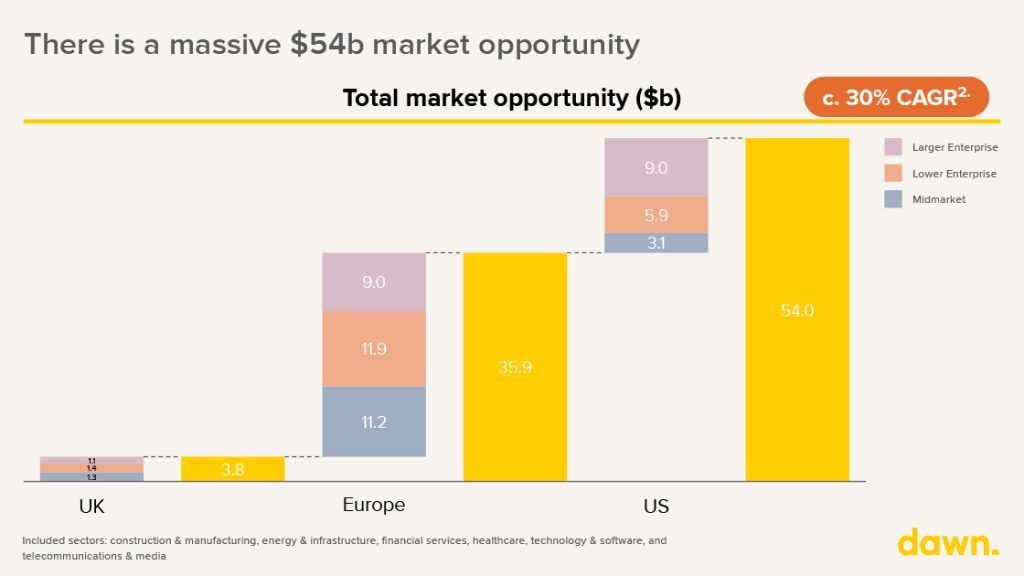

There is a large market opportunity here, and it is growing fast. We estimate that the market is at least $54b in the UK, Europe and the US, with strong demand across enterprise and midmarket companies. This demand also cuts across multiple sectors.

But the main prize isn’t the size of the addressable market – it is the share of enterprise change that can be captured when “software work” shifts from a specialist bottleneck to a repeatable operating capability. By compressing build cycles, enterprises can reduce costs, unlock more iteration, faster operational improvement, and new classes of internal products that were previously uneconomic.

The demand is real, but enterprises remain structurally under-resourced. They lack the talent and the capacity to translate business intent into production systems at speed. And, even when they can build, they run into the next wall: most of the value in enterprise AI is not generic. It is custom. CIOs increasingly view “custom AI” as the next big thing, and buyers are explicitly saying they need customisation to get value rather than buying narrow solution vendors that require endless extensions.

Why most pilots fail

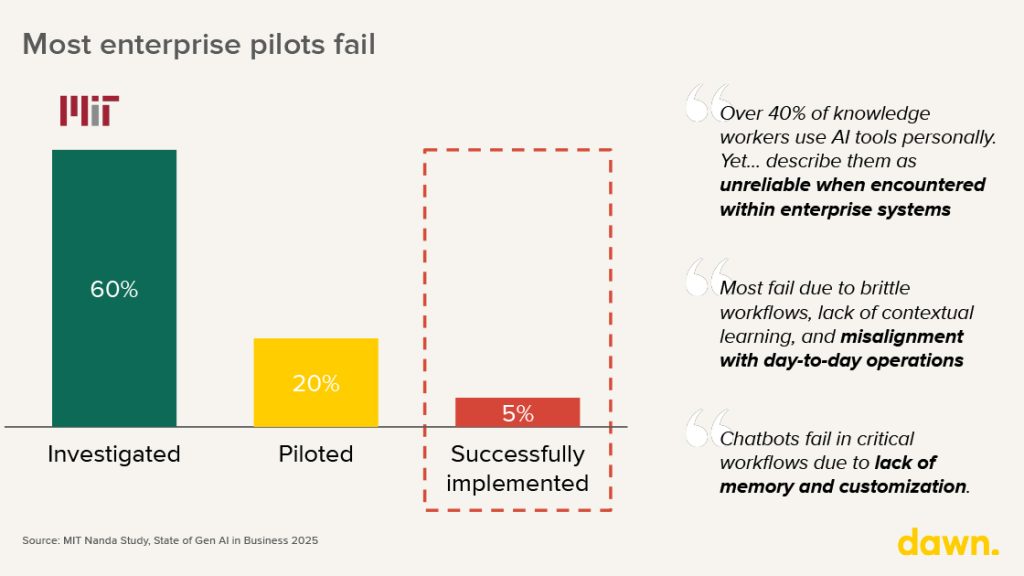

The harsh truth is that a lot of enterprise AI never makes it past the pilot stage. As an MIT Ananda study points out, there is an unfortunate funnel where 60% of projects are investigated, 20% are piloted, and only 5% are successfully implemented. The reasons cited for this are telling: brittle workflows, lack of contextual learning, and misalignment with day-to-day operations. Even when knowledge workers use AI personally, they often describe it as unreliable inside enterprise systems.

Enterprises typically fail at three points.

First, they underestimate data integration: customer records are spread across CRMs, ERPs, and legacy databases that were never designed to talk to each other, and in some industries the most critical data still lives offline or in proprietary formats. Second, they treat the AI application as a standalone product rather than embedding it into existing workflows, which means the people who are supposed to use it see it as extra work rather than better work. Third, they lack the governance infrastructure to move from experiment to production: no clear ownership, no model monitoring, and no audit trail. The result is a graveyard of impressive demos that never survived contact with operational reality.

How the competitive landscape is evolving

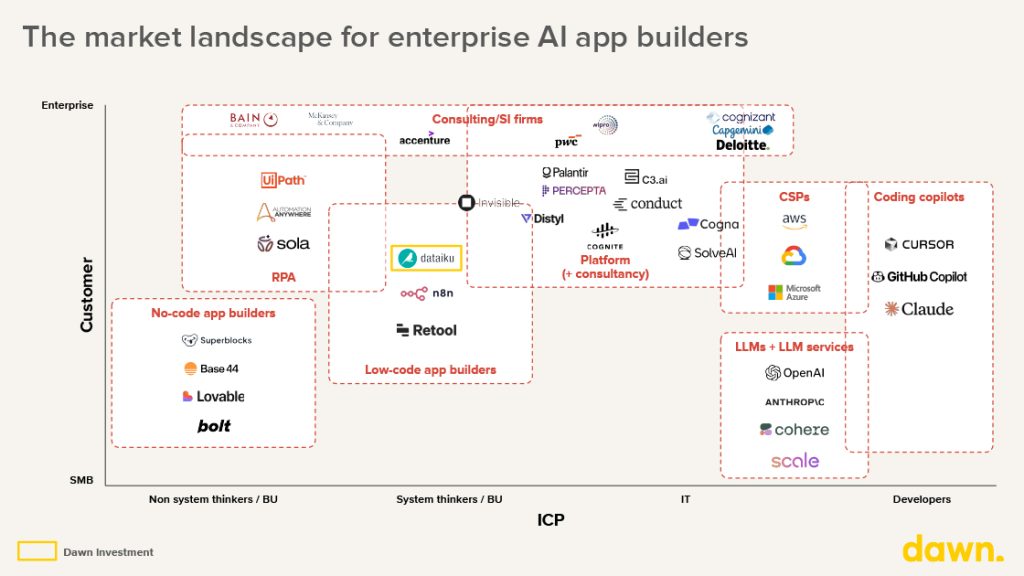

The market opportunity is enormous, so the competition is red-hot. We see the landscape splitting along two axes: who the user is, and how close the product sits to production systems.

Platform-plus-services players (for example Palantir, Distyl, Invisible Technologies, Cogna, SolveAI, Conduct) compete on their ability to translate enterprise complexity into deployed outcomes, not just developer productivity. At the same time, the lower-context end of the market will keep expanding via copilots, no-code builders and agent builders, because prototyping is now essentially free.

What it will take to win

We believe the companies that will win in this space will become the default data layer for their customers. They will need to ingest customers’ data and interpret how each organisation actually works. They will work with data models, process exceptions, permissioning, legacy systems, and – crucially – the politics of change. Being able to execute this successfully is the difference between prototypes and production. We believe data within context will remain the enduring moat.

Once companies are on track to securing this, we see many practical ways for startups to deepen their moat:

- Go deep in a vertical by selling applications that produce high ROI in repeatable domains. Here we have seen companies build durable moats by consolidating use cases across singular verticals. Outstanding examples have included financial services, oil & gas, manufacturing – industries with custom workflows that benefit from specialism and focus. Our portfolio company Quantexa, for example, works with 75% of the world’s biggest banks, serving multiple mission critical use cases from anti-money laundering to customer intelligence.

- Build cross-vertical capability that becomes an enterprise standard for building, deploying, and governing AI-enabled workflows. Here, horizontal excellence is required to enable high quality app building across different industries. Our portfolio company Dataiku, for example, provides broad based generative AI, analytics and ML solutions to 25% of the Fortune 500. They sell a platform that enables many kinds of use cases.

- Distribution through the builders of enterprise reality. The most credible routes to market often run through channels that already implement change: system integrators, cloud providers, strategy consultancies, and major application ecosystems. Partnership-led distribution and integration can help break through enterprise noise. Our portfolio company Blackwall is successfully reaching millions of small and mid-market customers via hosting providers, who are already the channel of choice for small companies.

We’re excited to partner with the teams shaping what the next generation of enterprise AI will look like. If you’re one of those teams, please reach out! You can find us at shamillah@dawncapital.com and alexandra@dawncapital.com.