Managing finances is complicated: incomes, outgoings, pensions, mortgage, savings, investments, children, parents, credit cards, car finance.

Imagine, for a moment, that hours currently spent on personal financial administration could be done by with the help of an autopilot. Seamlessly, painlessly — perhaps even profitably. A pay cheque arriving in your current account could be allocated and directed automatically with the right proportions heading to pay debts, cover daily expenses, or add to savings. Savings could be optimised to flow to accounts generating the highest returns, to offset mortgage payments, or automatically transferred to avoid accidental overdraft fees.

The same could happen with outgoings: debts automatically refinanced at the most competitive rate; bills processed; the cheapest utilities provider selected by default; home and car insurance compared or renewed automatically; duplicate subscriptions detected and cancelled; even payments processed in the most efficient way, to optimise rewards and avoid any nasty fees.

Where are we now?

Today, this blissful vision still sounds almost like science fiction. Despite all of the progress in digitising banking, day-to-day finance remains a chore.

However, fintechs have been making important steps towards automation. For some time now, robo-advisors have been automating investments into low-cost index trackers, guided by customers’ risk-tolerances and financial goals. Round-up savings offered by companies such as Moneybox and a number of neobanks are helping savers to stash away their spare change. Now in the US, Wealthfront has launched ‘Self-Driving Money’, promising to optimally allocate income across spending, savings and investments.

Innovation in areas such as machine learning is also enabling personal finance management (PFM) tools to graduate from simple but impractical, high-touch budgeting tools — pioneered by companies such as Mint — into autonomous platforms that require more limited manual intervention.

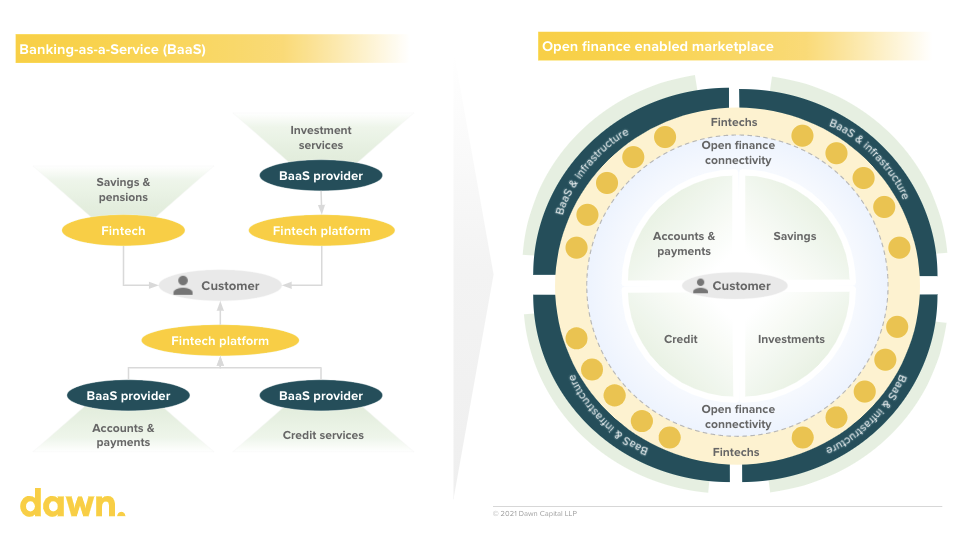

Nonetheless, providers today are still largely operating in single areas of expertise, partly due to the burden of acquiring and managing multiple regulatory licences. This means that autopilot functionality has also tended to take place within a bubble, both operated by a single provider and within a single aspect of a customer’s financial life.

What do we need?

Some providers have started to move horizontally, re-bundling financial products to provide a more holistic proposition. This is helped by increasingly mature banking-as-a-service (BaaS) propositions that enable customers to embed discrete financial products into their offering. Cloud-delivered API-led platforms are abstracting complexity of an infrastructure build, and even regulatory licensing, for services such as accounts, card issuance, payments, KYC/AML, and even brokerage services.

In the US, we’ve seen the emergence of new infrastructure marketplaces, like Bond, which allow companies to access and build on the infrastructure of a selection of different financial services providers. Meanwhile, Stripe has, almost inevitably, extended its merchant proposition and moved into the BaaS space with Stripe Treasury — delivering accounts with Goldman Sachs and Evolve Bank via its API — as well as Capital for Platforms, an embedded lending offering underwritten by Celtic Bank in Utah, which powers propositions such as Shopify’s Balance.

All this is reducing the time and cost for companies to release and offer new financial products. But for the end customer, they’re effectively becoming more tied in to a single vendor ecosystem, utilising services that are controlled and orchestrated by one central provider.

The promise and ambition of self-driving money should surely be wider than this. Ultimately, self-driving money should be about empowering the consumer with choice.

This is the promise of open finance. It envisions the possibility of a common data fabric that ties together financial services providers and enables seamless integrations between them. It’s this data network that will ultimately enable true autonomous platforms to emerge, optimising a customer’s financial life across multiple providers in a wide connected marketplace of financial services providers.

On the right track

Seeing this realised is still some way off — but there’s momentum building and perhaps reason to believe it will be with us sooner than we expect.

Looking back, 2020 was a huge year for the progression of open banking, evidenced by Visa’s attempt to buy California-based API startup Plaid for $5.3bn. Visa clearly saw Plaid’s data connectivity capabilities as strategic to its ‘network of network’ strategy. But, following the US Department of Justice (DoJ) suing to block the sale on antitrust grounds, the deal was called off in early 2021 and the company now intends to go public.

The saga served to highlight the disruptive potential of open finance. Today, Plaid provides bank account connectivity and validation. In future, it could potentially offer identity, credit scoring, and payments initiation services and more — services which could pose an existential challenge to the payments giants. Indeed, one executive cited by the DoJ likened Plaid’s potential threat to Visa’s online debit business as a ‘volcano’ whose tip today was only just showing above the water.

And there are other reasons for optimism. In the UK and Europe, adoption of open banking has been accelerating — and quickly. In our own portfolio, Tink has seen an explosion of activity across its network, supporting a widening range of use cases, from powering ABN Amro’s Grip app (incidentally now the top-ranked PFM app in the Netherlands with 670,000 downloads so far) to processing more than a million payments a month for companies like Kivra, a digital mailbox provider in Sweden, and Lydia, the leading French fintech.

More than two million people in the UK are now users of open banking, a doubling of the user base in just the last six months. One hundred and thirty nine providers have acquired TPP licenses in the last year to start building open banking products. This progress has been achieved even though currently, only access to transactional accounts is covered by the regulations.

How to ramp up

Consider how much more could be done for customers if savings, investments, pensions, mortgages and insurance services were also opened up. The UK and Europe, where open banking has been largely driven by regulators, has an opportunity to be at the forefront of a decade-long revolution. Lessons can be taken from the rollout of open banking and applied to the development of a broader open finance ecosystem. Regulators and the broader financial ecosystem must continue to pursue a common vision in partnership, pushing its frontiers.

The momentum is there. The UK’s Financial Conduct Authority (FCA) launched a consultation in December 2019 (it closed to new comments in October 2020) seeking new ways to encourage the development of open finance. EU regulators are doing likewise with the European Strategy for Data and a Retail Payments Strategy for Europe. Strong regulatory directives that set clear standards will be crucial to success — the industry discovered what a lack of directives in Europe have done in holding back progress, even as the UK raced ahead with clearer guidance for the CMA9.

As we move further into 2021, we expect to see more and more success stories adding to this momentum. Many feared open banking would create disruption for their business models; in reality, banks are seeing the benefits, with open banking products demonstrably driving customer value and loyalty, and reducing costs. Wider adoption of API standards through the UK suggests that the industry understands this and, as such, we’re seeing products and services built on top of open banking becoming table-stakes for retail and SME propositions. Meanwhile, big tech companies adding broader embedded financial solutions to their platforms are opening up the eyes of consumers and businesses to the benefits of a more open and interconnected ecosystem.

There remains a long road ahead. The industry is laying the foundations to turn the science fiction vision of autonomous personal finance into a reality — but we can go further, and faster. For founders in this space, the opportunity is wide open: this is no longer about building simply to meet and capitalise on regulatory requirements; it is building to meet growing consumer satisfaction and need.

For some other great articles around these topics, see:

- Fintech: The 2020s

- Fintech: The Fourth Platform

- Every Company Will Be A Fintech Company

- The Next Generation of Fintech Infrastructure

If you’re building in this space and would like to chat further, I’m dan@dawncapital.com