As we head into the 2023 budgeting season for tech startups, it’s becoming clear that nothing is clear in deciding between growth and cash preservation. Since the tech market crash earlier this year, much of the advice from VCs to startups has been around cash preservation — mostly that having a long runway was in of itself the answer. Initially, the popular number for a ‘responsible’ months of cash was 24. More recently we hear that “36 is the new 24”.

Two obvious problems. One is that for every month that passes, that number will go down, so it’s unclear if companies should keep cutting burn or dare to drop below 24 months of cash. The other problem is that all startups are treated the same — whether they’re killing it or getting killed, or in between.

In fact, the deeper problem is that in getting you two years of life, this approach doesn’t provide any guidance as to how those two years should be lived. Granted, for the small subset of late stage businesses, the goal of gracefully growing to profitability without more capital is a real option. But the reality for the great majority of smaller startups is that aiming to be a sub-scale, low growth, profitable business is not attractive for founders and investors alike. So where to from here?

A little recent history…

The last few years in startup land has been the story of cheap capital which, as I have written before, has led to startups making the rational and right decision to grow with little regard to efficiency. However, now that fundraising is much tougher, valuations have come down, and cash on the balance sheet forms a far more important part of a company’s value, startups with high burn are literally burning their equity — unless they are creating demonstrably far more value for the cash they are burning. Last year, the yardstick by which to measure value creation was crystal clear — growth. In today’s environment it couldn’t be less clear. Startups can’t hope to be even in the postcode of the rule of 40 at low scale, so they are grappling to understand the trade-off between growth and efficiency, and what it means for their next fundraise years away in a foggy environment where many VCs are not transacting.

So the prevailing answer has been to trim companies a bit everywhere to mathematically force the cash balance divided by monthly burn to equal 24 — or 36. Companies might start cutting into their Sales and Marketing teams, leaving just enough quota capacity in today’s slower growth environment to hit next year’s numbers. Then, if more burn reduction is needed, the cuts come out of Engineering and Product.

This one-size-fits-all approach will lead many companies to cut again and again to manage a shrinking cash balance, killing the most powerful employee retention tool companies have — business momentum. Without momentum, the opportunity cost induces key talent to leave, hence the business further underperforms, new funding becomes unlikely, and the company spirals downwards into irrelevance.

A different approach…

Instead of one-size-fits-all, depending on performance, we at Dawn recommend that companies place themselves into one of three buckets, ordered by decreasing company performance.

1. Shoot the Lights out: For a very small subset, fundraise right now and invest heavily in current success

2. Steady as you go: Fundraise thoughtfully and grow efficiently

3. Reboot: Zero Based Budgeting

Bucket 1…

The first thing to notice is that two of the strategies involve fundraising (full disclosure, I get paid to invest). As the VC market is currently very slow, the first quarter of 2023 is probably the first viable window to fundraise. This is contentious advice and I can hear a cacophony of voices urging CEOs to instead spend their cash wisely and grow into their valuations, to keep their heads down and execute — and to keep away from VCs. I say, don’t be an ostrich. I get it that founders scored great financing deals over the last couple of years. Congrats. Get over it. And don’t let past successes stop you stealing share and building a category leading business when others are cautious. So for businesses that are performing strongly, the most pragmatic route is to take that insider money that should be chasing you and step on the gas (full disclosure #2, my colleagues and I would love to join your insiders in backing you). A glide path to eventual profitability or rule of 40 is still needed even for these companies, but they are afforded a lot more flexibility on the journey there.

Bucket 3…

At the other end of the scale, there are businesses that are unfundable now and for some time to come, but their CEOs don’t know it as they have disengaged from the funding market, hiding behind piles of cash. Understandably, these CEOs are nervous at having external scrutiny of their business at a time when they’re underperforming. However, better a reality check now than when there is no cash. For those CEOs that know that their business is currently unfundable, the third option, zero based budgeting is the right but painful option that management needs to get to quickly. Starting from 0 headcount and carefully justifying adding each incremental head commensurate with the current momentum of the business. A radically reshaped business with tangible momentum in whatever it chooses to refocus on (product or GTM) and cash in the bank is a better business.

Bucket 2…

Most CEOs I see are trying to position their business in bucket 2 — grow efficiently. They see this as the “keep optionality” bucket. In my experience this optionality is actually indecision. If there was ever a time that calls for clear strategic choices and focus, it is now. Furthermore, it’s not clear that any optionality is actually created. Companies get locked into a given path sometimes without realising it. Tightening budgets make it very difficult to maintain product leadership and commercial market coverage at the same time. Going for this option when you actually belong in bucket 3 is the surefire way to end up in the death spiral I talked about in the beginning of this post. On the other hand, if you are at scale (>$10m ARR) and can grow at 30–50% with solid capital efficiency (>0.7x) and near breakeven then this is the right option. Externally, there are smart, credible investors that look to make new investments in such “good” companies at “fair” valuations with the ambition to sell them on to private equity investors or strategics at a target IRR carefully weighing the company’s investments along the way. This is actually the good outcome for the overwhelming majority of startups that don’t fail. However, it’s probably more likely that a “nothing-to-lose, refocused bucket 3 company with cash” has a heroic result than one that embarked down the PE journey.

The hard bit…

So that was the easy bit. The hard bit is for founders, managers, investors and boards to objectively agree which bucket their company should sit in.

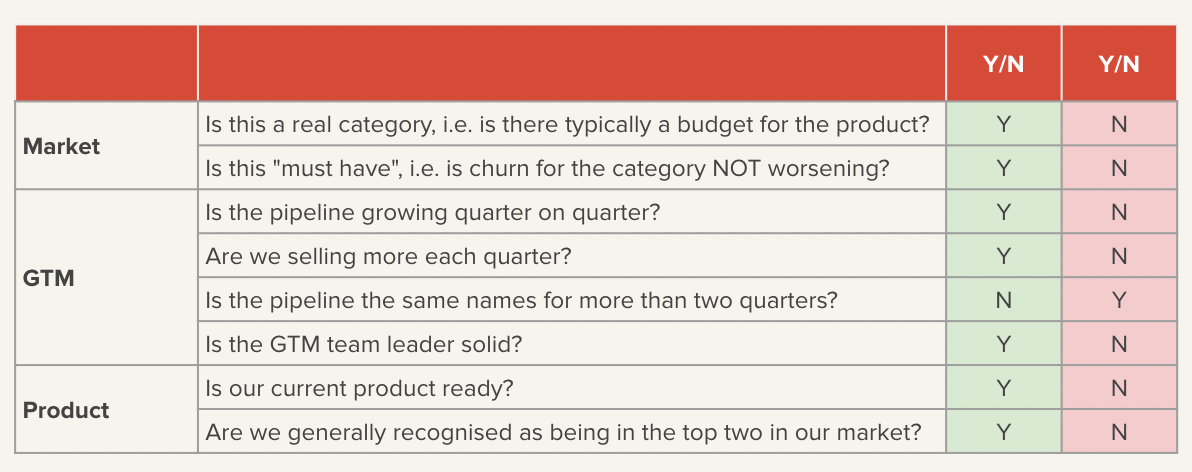

The really easy bit…

To help assess the current potential of a business we have included below a quick and dirty model with very simple yes/no questions that can help to drive to an answer. If the 3 areas of Market, Product and GTM are all green then you’re in bucket 1. If more than one section — say Market — is red, then bucket 3.