The venture debt industry has seen eye-watering growth over a decade-long bull run. In the US alone, volumes rose from $6bn in 2015 to $10bn in 2019, according to research from Kruze. And on the back of this, a vibrant ecosystem of lenders, advisors, brokers and service providers has sprung up to support this rapidly growing market.

But Covid-19 may put a dampener on the party: many in the venture debt ecosystem haven’t weathered a storm like this before. There’s a host of guides and conventional wisdom about raising venture debt in good times, but we believe we still need a framework for thinking about it in a Covid-19 world.

We’ll start by considering what’s changed and what hasn’t in this new economic reality. Next, we’ll set out a framework for thinking about whether your business could and should raise venture debt to weather the crisis.

Some things have changed

There has been a flight to quality across both debt and equity. While lenders may be hesitant to admit this, the bar is higher for raising new debt. There is greater scrutiny of business models and operational efficiency, and diligence processes are longer and deeper, not helped by the fact that we all now work remotely.

In addition, lenders are now solving to get through Covid: no longer is it good enough to be bridging to a supposed near-term equity round. Typically, lenders are now looking for 18 months of cash runway post-financing (to get businesses past the eye of the storm) and expect cost bases to be rationalised and efficient.

We’re seeing increased risk aversion reflected in terms in some cases, with lenders trying to lock in returns by limiting flexibility around fees, warrants and draw schedules.

But most things have not

Despite the above, the fundamentals around thinking through venture debt remain the same.

First, debt must be a bridge to somewhere. It should never be seen as a panacea, but instead as part of a balanced capital structure. A well-negotiated package can lower WACC, benefiting founders, employees and investors. But, unlike equity, debt incurs a near-term cash cost and is secured over company assets. Any debt needs to bridge to a place where metrics will deliver a realistic post-Covid fundraise — this could be creating a more diversified revenue base, launching a new product, supporting initiatives to reduce burn, or hitting profitability/exit. The decision process requires careful mapping of milestones and fuel stops over the next 24 months.

If you have existing debt, review whether current resources will get you to these milestones. Many lenders acted fast: Silicon Valley Bank, for example, quickly announced a six-month capital repayment holiday and other measures to support clients through the downturn. Key terms to revisit with your lender could be drawdown and repayment schedules, as well as performance milestones for additional tranches.

Second, not all debt packages are created equal. There is a big difference between a package with favourable terms versus a package with unfavourable terms. And debt is not right for every business — the details matter. Packages need to be properly modelled out, as there are individual dynamics for every company, particularly around the cash collection profile. Levers like interest rate, repayment holidays, warrant coverage and covenants can determine whether venture debt really makes sense or not.

Third, venture debt typically needs legs to stand on. It must be complemented by supportive equity investors and a cost-efficient, well-managed business. Without these legs, debt will be difficult or impossible to raise today on terms that make sense. But if well negotiated and used alongside an aptly-sized cost base, it could buy you three to six months of runway.

Raising from a position of strength

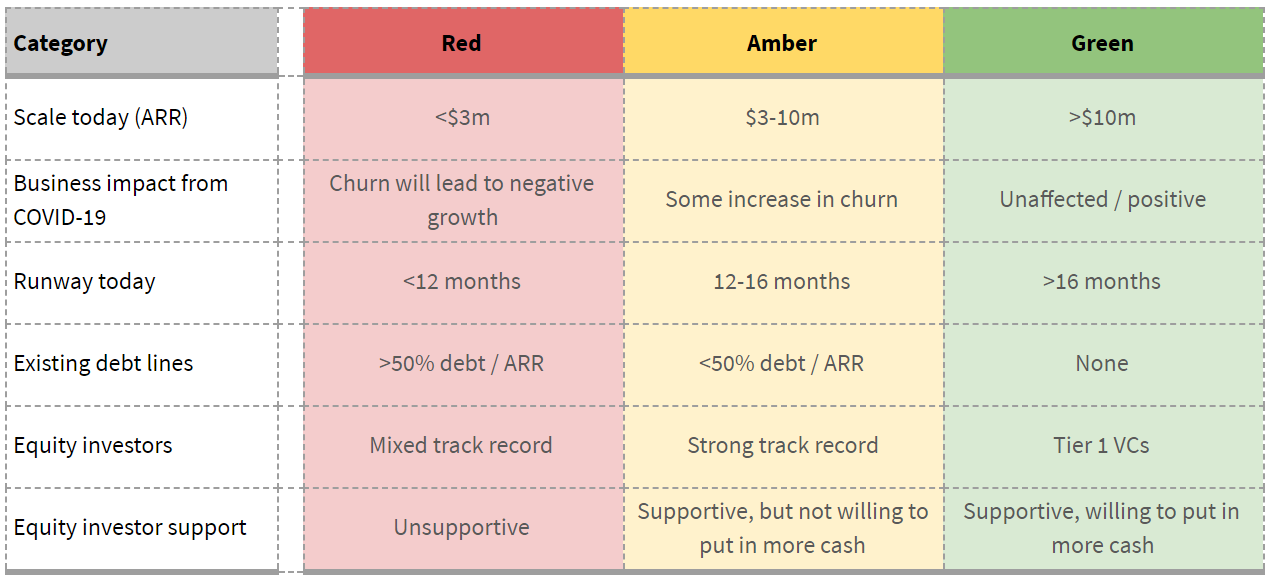

As a rule of thumb, venture debt should be raised from a position of relative strength. This is what will increase the odds of securing a package that is a support rather than a burden. Below is a back-of-the-envelope framework for thinking today about your company’s ability to raise debt on favourable terms.

The top three categories — scale, Covid-19 impact and runway — deal with the company’s fundamentals and its balance sheet, the most crucial factors at present. The bottom three — existing debt lines, equity investors and equity support — deal with the current sources of financing, also important factors for lenders.

If mostly towards the green zone: venture debt may be a helpful addition to your capital structure and it’s likely worth reaching out to lenders to understand what is available. If mostly towards red: if you can raise debt at all, it will likely be on poor terms and potentially more of a burden than a support.

Making the right decision — the details matter

As a next step, assess your current financial resources and whether they will get you to your next key milestone — ideally without having to go out to raise equity during the downturn, or with messy metrics a few months after. If there is a gap, consider whether you can raise venture debt on favourable terms and speak to lenders to understand what is available.

To summarise, while Covid-19 is ushering in a new economic reality, we think the core building blocks for thinking about venture debt have not changed. Raising debt is not always the right decision: it must be a calculated bridge to somewhere, not all packages are created equal, and it must be accompanied by supportive shareholders and an efficient cost base.